You likely interact with insurance more often than you think. From your car to your health, or even your home, insurance plays a vital role in protecting us from the unexpected. But have you ever truly stopped to consider how it works or the different ways you can secure coverage? Let’s dive in and demystify the commercial insurance industry!

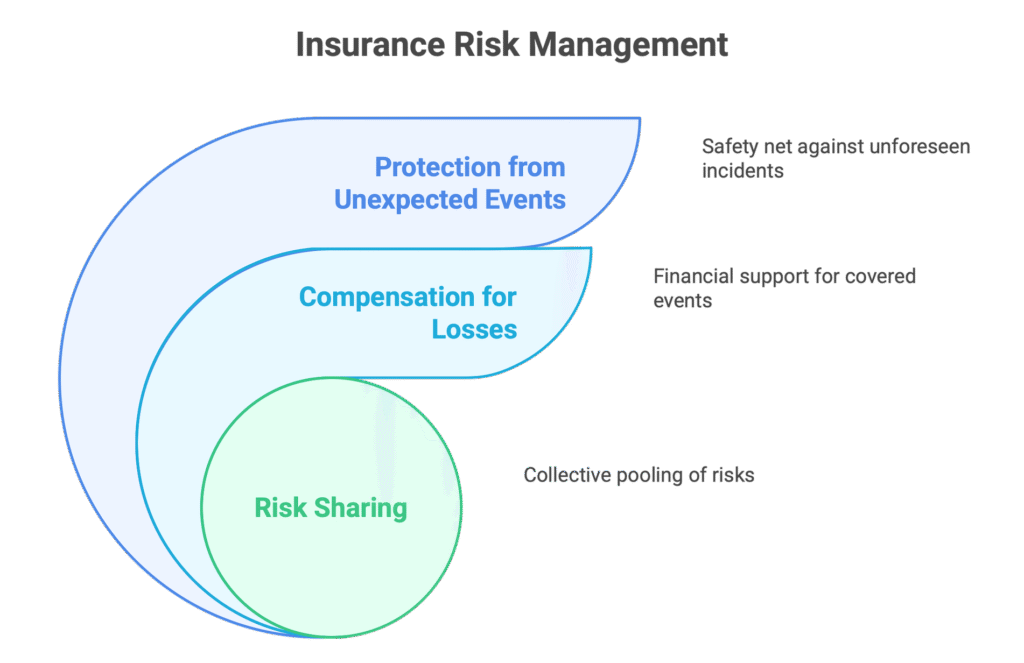

The Core Purpose of Insurance: Sharing Risk and Covering Losses

At its heart, insurance serves two fundamental purposes:

It allows you to share the risk of unforeseen negative events before they happen.

It provides compensation for losses that occur due to covered events.

Instead of solely relying on your own financial resources when something goes wrong, insurance enables you to pool risk with many other customers. This collective approach means you’re not alone in covering expenses if an incident occurs. Think of it as a safety net that’s collectively funded.

How Do People Buy Insurance? More Options Than Ever!

Thanks to the digital age, customers have a wider array of options for purchasing insurance today. Here are some of the most common avenues:

•Brokers (Independent Agents): These professionals represent multiple insurance carriers and work on your behalf as the customer. They assess your needs, offer advice on necessary coverage, and compare rates across various providers.

•Managing General Agents (MGAs): Similar to brokers, MGAs also represent insurance companies. However, they possess underwriting and binding authority directly from the insurers they work with.

•Captive Agents: Unlike brokers, captive agents work exclusively for one specific insurance company, selling its policies directly to customers.

•Direct-to-Consumer Websites: Many insurance companies now allow you to purchase policies directly through their own websites.

•Online Marketplaces: These platforms operate much like online brokers or MGAs, listing policies from multiple carriers in one convenient digital space.

•Banks and Retail Outlets: Some insurance companies form business-to-business relationships with other entities, like banks or retail outlets, allowing them to function as insurance agents.

• Employer Plans: A very common way to obtain insurance, employer plans typically include medical and dental coverage. They can also extend to life, disability, and long-term care insurance

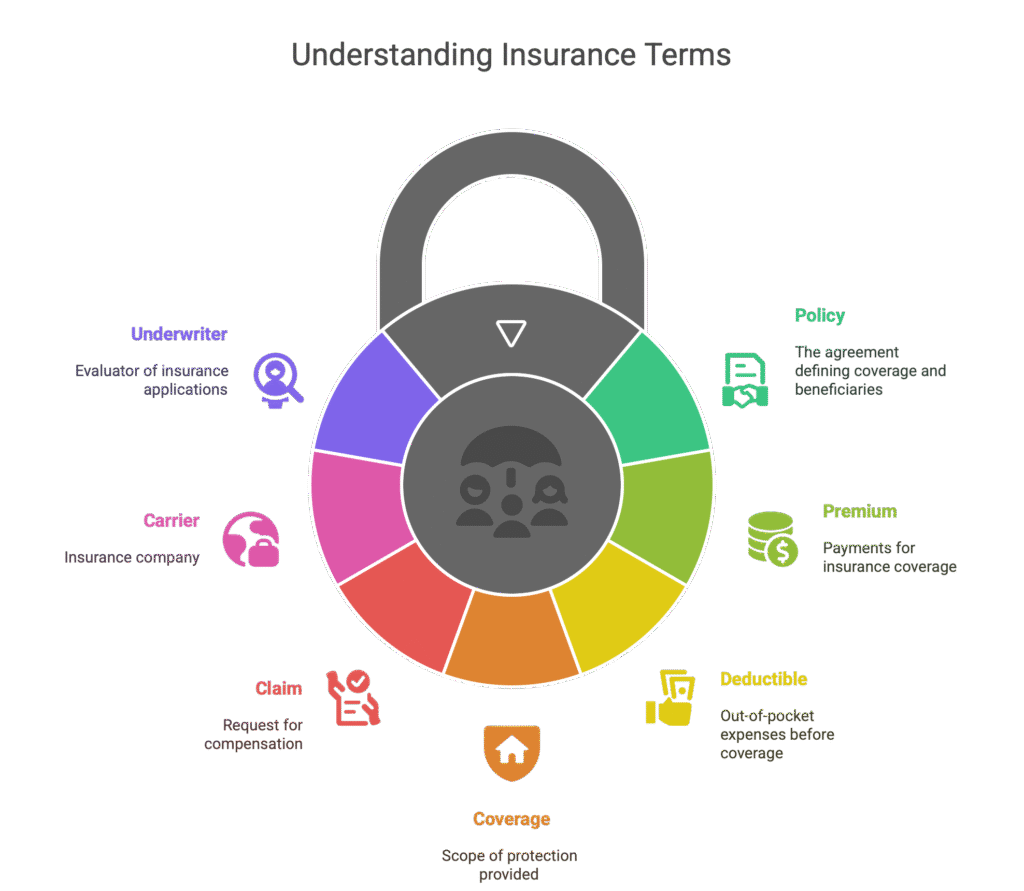

Essential Insurance Terminology to Know

Understanding the language of insurance can significantly improve your ability to communicate effectively with industry professionals and make informed decisions. Here are a few key terms:

Policy: This is the agreement between an insurance company and a client that clearly defines what is covered and who the beneficiaries are.

Premium: The payment you make to the insurance company for your coverage. This payment can be made monthly, quarterly, or annually.

Deductible: An amount you, the policyholder, must pay out-of-pocket before your insurance coverage starts to provide compensation.

Coverage: This refers to the scope of protection provided by your policy, including the specific risks insured against and the properties, locations, or individuals covered.

Claim: A formal request for compensation submitted to the insurance company when a covered event occurs.

Carrier: Simply put, this is another term for the company that sells insurance. You might also hear them called a “provider” or “payer”.

Underwriter: An insurance professional whose job is to review and evaluate insurance applications. They determine the coverage and premium that should be offered to a customer based on various factors.

Empower Yourself with Knowledge!

The better you understand the commercial insurance industry, the more effectively you can navigate your options and secure the protection you need. By understanding how insurance functions, the various ways to buy it, and key terminology, you’re better equipped to make informed decisions for yourself and your assets.